Common Options-based Strategies

By Eric McArdle on Jan 13, 2026

Once you understand the four core positions—buying and selling calls and puts—you can begin combining them to shape different risk and return profiles. Spread and combination strategies use two or more options on the same underlying asset to adjust exposure, manage cost, or structure how an investment may respond to various market conditions. These approaches can be designed to address a range of objectives, such as participating in price movement, reducing directional risk, or defining potential gains and losses

Covered Call

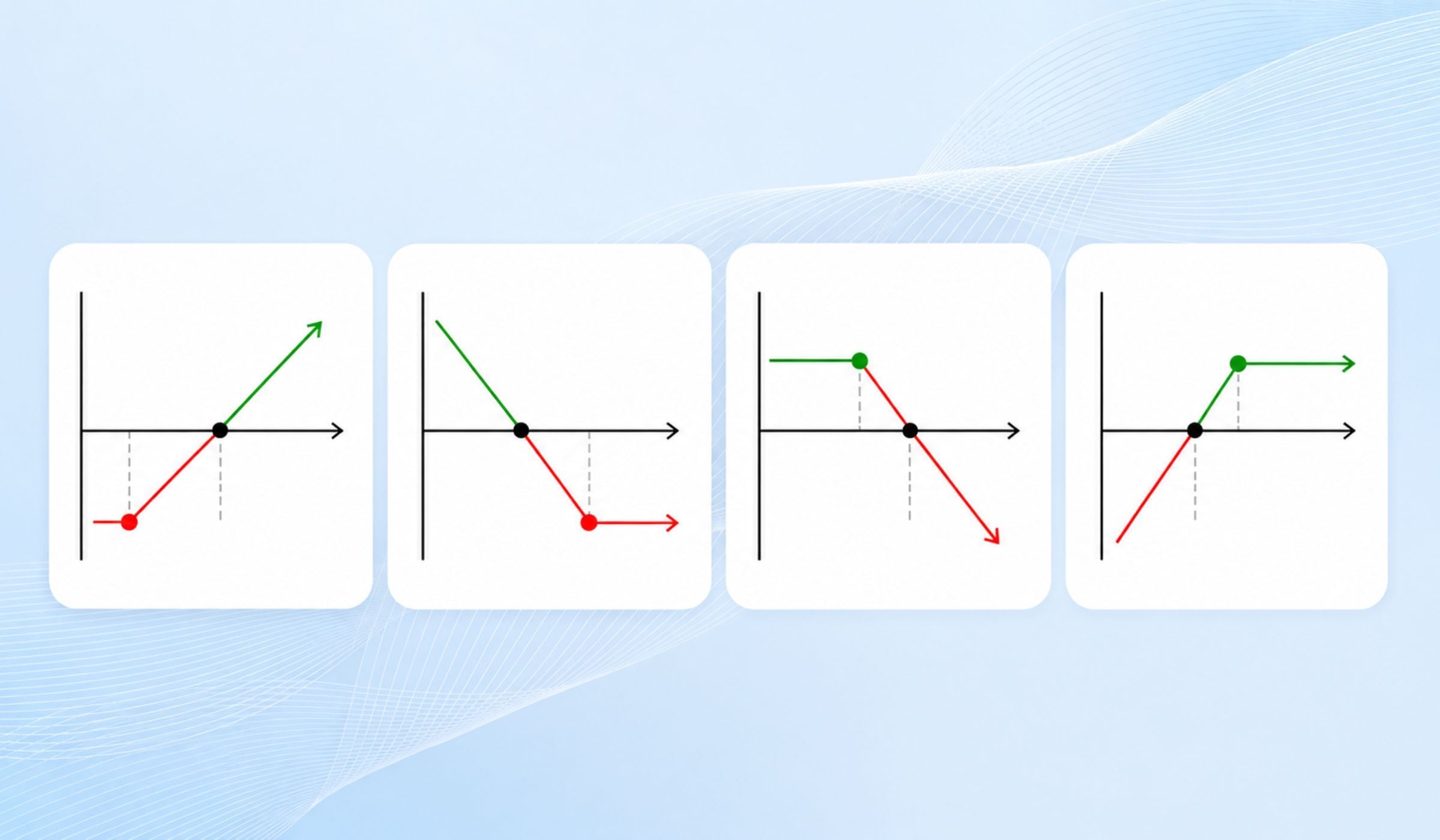

A covered call pairs ownership of the underlying stock with selling a call option on those shares. The position is commonly used to generate premium income while holding the stock, with the trade-off that upside potential becomes limited by the strike price of the written call.

-

Generates premium income when the stock stays flat or rises modestly, allowing the call to potentially expire worthless while the shares are retained.

-

Upside is capped at the strike price, because the shares may be called away if the option is exercised.

-

Premium received provides partial downside offset, though the stock can still decline in value.

-

Good when: You anticipate limited to moderate upside and are comfortable with the possibility of selling your shares if the stock reaches the strike price.

-

Bad when: The stock rises sharply or if you prefer to retain full upside participation; the position may be assigned, and gains above the strike price are not captured.

This is a popular income strategy for long-term investors who are comfortable giving up some potential upside in exchange for steady cash flow.

Protective Put

A protective put pairs a long stock position with purchasing a put option. The put establishes a defined floor on potential losses while allowing the stock position to remain fully invested.

-

Limits downside risk below the strike price, since the put can offset losses if the stock declines.

-

Maintains full upside participation, as gains in the stock are not capped.

-

The cost of the put reduces overall returns, because the premium is paid upfront and may expire without being used.

-

Good when: You want to define potential downside risk while continuing to hold the stock and expect near-term uncertainty or market volatility.

-

Bad when: The cost of the put is elevated or the stock rises steadily; the premium reduces net returns and the protection may expire without providing offsetting value.

A protective put defines how much downside risk you are exposed to by setting a predetermined level at which losses can be offset. You pay a premium for the put, which establishes a floor on potential losses while allowing the stock position to remain fully invested.

Vertical Spreads

A vertical spread involves buying and selling the same type of option (either both calls or both puts) with the same expiration date but at different strike prices. Vertical spreads are defined-risk strategies that express a directional view while limiting both potential gains and potential losses.

-

A Bull Call Spread is constructed by buying a call at a lower strike price and selling another call at a higher strike price. The position benefits when the stock rises toward or above the higher strike. The premium from the short call helps reduce the net cost of the long call, while also setting a maximum profit at the upper strike. The maximum loss is limited to the net premium paid.

-

Good when: You expect a moderate rise in the stock and want to lower the cost of a long call position while being comfortable with a defined profit cap.

-

Bad when: The stock remains below the lower strike or rises sharply beyond the sold strike; the spread may expire worthless if the move is insufficient, and gains above the higher strike are not realized.

-

-

A Bear Put Spread is created by buying a put at a higher strike price and selling another put at a lower strike price. The position benefits when the stock declines toward or below the lower strike. The premium received from the short put reduces the net cost of the long put but establishes a maximum profit for the spread. The maximum loss is limited to the net premium paid.

-

Good when: You expect a modest decline in the stock and want a bearish position with defined risk and lower cost than purchasing a standalone put.

-

Bad when: The stock remains above the higher strike or declines sharply beyond the lower strike; the spread may expire worthless if the move is insufficient, and any decline beyond the lower strike does not increase the spread’s maximum value.

-

Vertical spreads are structured to express a directional view while defining both potential gains and losses. They are typically used when an investor expects a move in a particular direction but does not anticipate significant price swings beyond the strike range of the spread.

Straddles and Strangles

Straddles and strangles involve using both a call and a put option on the same underlying stock with the same expiration date. These strategies are designed to reflect a view that volatility may increase, regardless of direction.

-

Straddle: A straddle is constructed by buying one call and one put at the same strike price. The position benefits from large price movements in either direction. Both options carry time decay, and the combined premium can be substantial. Gains are theoretically uncapped on the upside and significant on the downside, subject to market conditions and liquidity.

-

Good when: There is an expectation of a significant price move in either direction, such as around key events, and the goal is to maintain exposure to a wide range of possible outcomes.

-

Bad when: The stock remains within a narrow range or implied volatility declines; time decay can erode the value of both options quickly.

-

-

Strangle: A strangle involves buying a call and a put at different strike prices, typically both out-of-the-money. The entry cost is lower than a straddle because both strikes are farther from the current price. The position requires a larger move in either direction to reach profitability. Exposure remains directional agnostic but more dependent on magnitude.

-

Good when: You expect elevated volatility but want a lower-premium alternative to a straddle and are less focused on predicting a specific direction.

-

Bad when: The underlying price does not move enough to offset the combined premiums or implied volatility falls; both options can expire worthless.

-

Buffer Strategies (e.g., Buffer ETFs)

A buffer structure typically uses options to absorb a predefined portion of downside movement while also limiting upside potential. The strategy often incorporates a combination of purchased puts to provide partial downside offset and written calls that cap upside once the stock or index reaches the call strike. The approach reduces losses only within a specific range; declines beyond the buffer range can still result in losses. Upside participation is limited because gains above the call strike are not captured. These structures are generally designed to create a more controlled return profile over a defined outcome period.

Long Put Protection

A long put provides the right, but not the obligation, to sell the underlying asset at a predetermined strike price during the option’s life. Downside risk is defined below the strike price, regardless of how far the underlying falls. Upside participation remains fully intact, apart from the cost of the put premium. The protection requires an upfront premium, which may expire without offsetting losses if the underlying does not decline.

Key Distinctions: Buffer Strategies vs Long Put Protection

-

Scope of Protection: Buffers cover a limited range of losses; long puts define a clear floor on losses at the strike.

-

Upside: Buffers cap gains above a predetermined level; long puts do not cap upside but reduce net returns by the premium paid.

-

Cost vs. Structure: Buffers embed the cost of protection in a multi-leg option structure; long puts require a direct premium payment.

-

Outcome Profiles: Buffer strategies smooth results within a set range over a defined outcome period, whereas long puts provide protection that responds directly to movements in the underlying asset.

Analogy: Protective Gear

A buffer works like bumper guards on a car. They help absorb smaller bumps and everyday impacts, but they are not designed to handle severe collisions.

A long put is more like a reinforced safety feature—such as a roll cage—that establishes a defined limit on how much damage you can experience in a major downturn. It offers broader protection than bumper guards, but comes with a higher upfront cost.

Short Options vs. Spreads

Selling options generates premium income, but it also exposes the seller to potentially substantial losses if the market moves sharply against the position. A short call can face theoretically unlimited loss if the underlying rises significantly, and a short put can face large losses if the underlying declines substantially.

A spread structure—where another option is purchased to offset part of this exposure—defines the maximum potential loss. The long option acts as a risk cap, reducing or eliminating the asymmetry present in standalone short positions. While this approach limits the total premium that can be collected, it creates a more balanced risk–return profile compared with selling an uncovered option outright.

Analogy: Driving Without a Seatbelt

Selling an option without a corresponding long option is like driving without a seatbelt. Everything may feel straightforward when conditions are calm, but unexpected events can lead to much larger consequences because nothing limits the impact.

Adding a second option to create a spread is similar to buckling your seatbelt. It doesn’t eliminate the possibility of a sudden move, but it sets a limit on how severe the impact can be by defining the maximum loss on the position.

Read more about Basic Option Strategies

Read more about What Influences an Option's Price

Read more about Covered Call vs Put Selling

This material is for educational purposes only and does not constitute investment advice or a recommendation of any security, strategy, or product.

Options involve risk and are not suitable for all investors. Prior to trading options, you should carefully read the Characteristics and Risks of Standardized Options (ODD), available from your broker or at www.theocc.com.

Liquid Strategies, LLC (“Liquid”) is an independent investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”) under the Investment Advisers Act of 1940, as amended. Registration as an investment adviser does not imply a certain level of skill or training. Additional information about Liquid, including our investment strategies, fees, and objectives, is available in our Form ADV Part 2A and Form CRS.

The information provided in this material is for informational and educational purposes only and should not be construed as investment, tax, or legal advice, nor as an offer to buy or sell any security, strategy, or product. The content is provided on an “as is” basis without warranties of any kind. Although the information has been obtained from sources believed to be reliable, Liquid does not guarantee its accuracy or completeness and it may be superseded by subsequent market events or other circumstances. Liquid undertakes no obligation to update or revise any information contained herein.

Options involve risk and are not suitable for all investors. Options can be highly volatile, may lower total returns, and even well-structured strategies may result in losses due to market conditions or unforeseen events. Short options strategies involve substantial risk and may expose investors to significant or unlimited losses. Before trading options, investors should carefully review and understand the disclosure document Characteristics and Risks of Standardized Options (ODD), available at www.theocc.com or from your broker.

Educational discussions of strategies—including covered calls, put selling, spreads, protective options, volatility strategies, or execution methods—are intended to illustrate general concepts only. These descriptions are not recommendations, and actual performance will vary depending on market conditions, liquidity, transaction costs, and individual circumstances. Analytical measures and sensitivities such as delta, gamma, theta, and vega estimate sensitivity to inputs but do not predict future results.

Analogies are simplified illustrations intended to help explain options concepts. They may not reflect all risks, characteristics, or market behaviors associated with actual trading or investment strategies.

Investing involves risk, including the potential loss of principal. Past performance is not indicative of, and does not guarantee, future results. No representation is made that any strategy will achieve profits or prevent losses. Investors should consult with qualified financial, legal, and tax professionals before implementing any investment strategy.

© Liquid Strategies, LLC. All rights reserved. Not for further distribution without prior written consent.

You May Also Like

These Related Stories

Covered Call vs Put Selling

Basic Option Strategies