What Is an Option?

By Eric McArdle on Jan 13, 2026

An option is a type of contract on an underlying asset (such as a stock or ETF). It gives the buyer of the option the right—but not the obligation—to buy or sell that asset at a specified price (the strike price) before or at a certain expiration date.

Every option trade has two sides:

-

The investor who buys the option is said to be “long” the option.

-

The investor who sells (or “writes”) the option is said to be “short” the option. Every option trade has two sides:

-

The investor who buys the option is said to be “long” the option.

-

The investor who sells (or “writes”) the option is said to be “short” the option.

-

The rights and risks are different for each side.

Calls and Puts

-

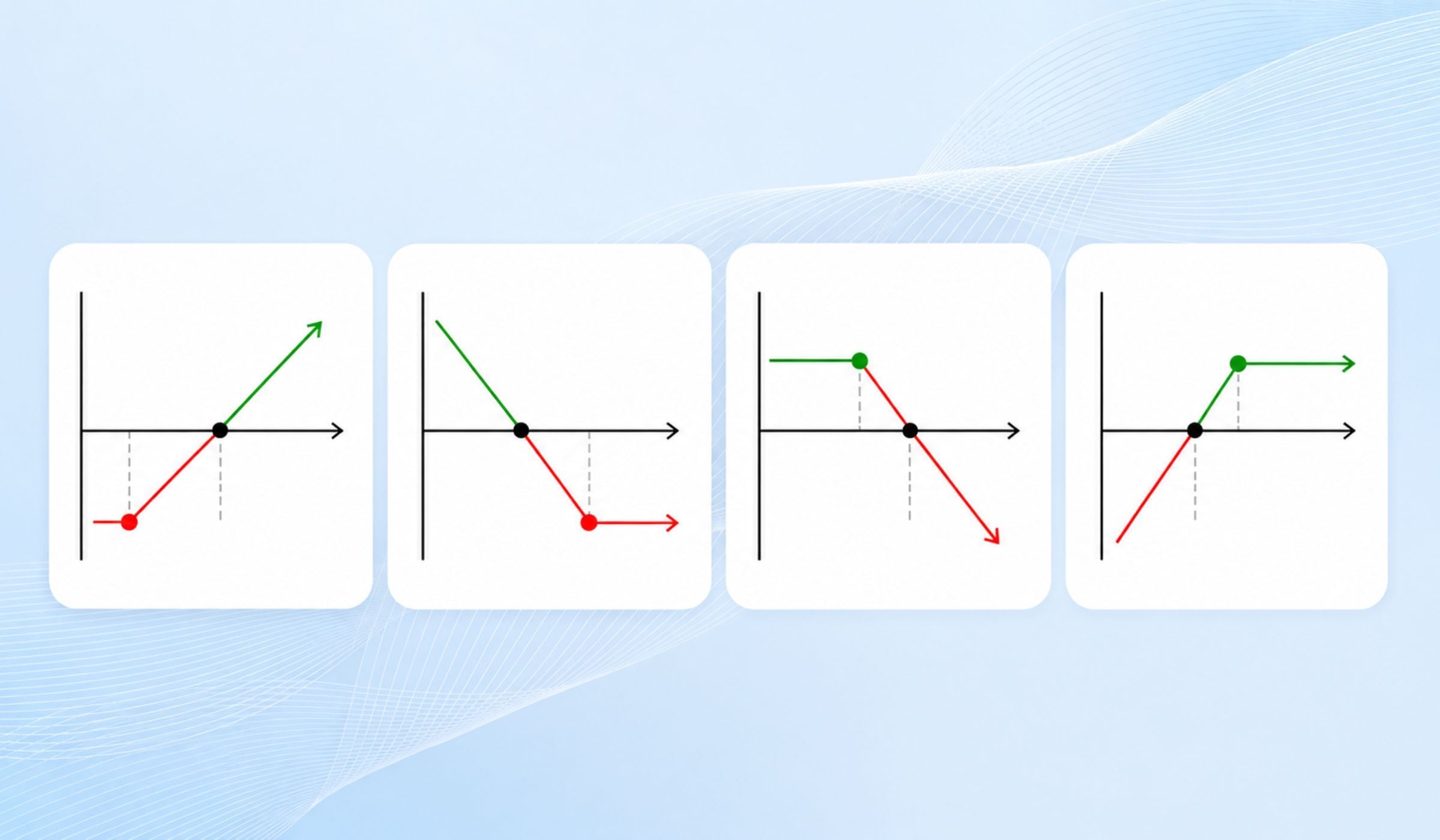

A call option gives the buyer (long call) the right to buy the underlying asset at the strike price.

-

The seller (short call) has the obligation to sell the underlying asset at the strike price if assigned.

-

-

A put option gives the buyer (long put) the right to sell the underlying asset at the strike price.

-

The seller (short put) has the obligation to buy the underlying asset at the strike price if assigned.

-

When you buy an option (take the long side), you pay a cost known as the option premium. The most you can lose on a long option position is typically this premium. You’re not required to take action if the market moves against you; you can choose whether to exercise the option or close it before expiration.

When you sell an option (take the short side), you receive the premium, but you take on an obligation. If the option buyer chooses to exercise—or if the option is automatically exercised at expiration—you may be assigned, which means you must fulfill the contract terms (buying or selling the underlying at the strike price). Depending on the strategy and whether the position is covered or uncovered, potential losses on a short option can be substantial and, in some cases, theoretically unlimited.

Once the expiration date passes, the option will either have remaining value or expire worthless. Assignment for short options can occur at or, in some cases, before expiration.

Why Use Options?

Investors use options in different ways, and the risk profile depends on whether they are long or short the contract, as well as on the overall strategy.

Some common reasons include:

-

Leverage

-

Options allow you to control exposure to an underlying asset with less capital than buying or shorting shares directly.

-

This leverage can magnify both gains and losses.

-

-

Defined Risk for Buyers

-

When buying an option (long call or long put), the maximum loss is typically limited to the premium paid, plus any applicable transaction costs.

-

When selling an option, risk may be greater and, for certain uncovered positions, can be significant or unlimited.

-

-

Flexibility

-

Options can be used to hedge existing positions, express a market view (bullish, bearish, or neutral), or seek to generate income (for example, through certain option-writing strategies).

-

Strategies that involve selling options to generate income also involve the risk of assignment and potentially large losses if the market moves against the position.

-

-

Optional Exit

-

Whether you are long or short, you may be able to close your position before expiration to realize a profit, reduce a loss, or manage your risk and assignment exposure. Liquidity, market conditions, and transaction costs will affect your ability to do so.

-

Analogy: The Car Lease (Long Side Focus)

Think of buying an option like leasing a car instead of purchasing it outright.

When you lease a car, you pay for the right to use it over a set period. You don’t own the car—you simply control it during that time. If you decide you no longer want it, you may be able to return it early (similar to closing a long options position before expiration). When the lease ends, your control over the car and your risk exposure related to that lease generally end.

In a similar way, when you are long an option, you pay a premium for temporary control over potential price movement, not permanent ownership of the asset. Once the contract expires, that control ends and the option is no longer valid.

By contrast, the party that is short the option is more like the leasing company: they receive the lease payments (the premium) but take on obligations and risks if the contract terms need to be fulfilled.

Analogy: The Price Promise (Short Side Focus)

Selling an option is similar to making a price promise in exchange for a fee.

When you sell an option, you collect the premium up front. In return, you agree that you will honor a specific price for a set period of time, even if market conditions change. Your potential profit is limited to the premium you receive, but your potential loss can be much larger if the market moves against you.

-

Short Put (Promise to Buy)

Imagine you tell a friend:

“For the next three months, if you decide to sell your car, I’ll buy it from you for $20,000. Pay me $500 now for that promise.”

If the car’s market value stays near or above $20,000, your friend is unlikely to use that promise, and you simply keep the $500.

But if the car’s value drops to $10,000, your friend will probably ask you to follow through. You’re now obligated to buy the car for $20,000, even though it’s worth much less in the market.

In a similar way, when you are short a put, you receive the premium today but may be required to buy the underlying asset at the strike price if assigned, which could be well above its current market value. -

Short Call (Promise to Sell)

Now imagine you own a popular game console and tell someone:

“For the next three months, you can buy my console from me for $300 any time you choose. Pay me $20 now for that right.”

If the console’s market price stays below $300, the other person may never use that agreement, and you keep the $20.

But if the market price jumps to $600, they are very likely to exercise their right to buy it from you at $300. You must sell at the agreed price and give up the additional amount you could have received at the higher market price.

Similarly, when you are short a call, you receive the premium but may be required to sell the underlying asset at the strike price if assigned, even if the market price has moved significantly higher.

In both cases, the person who sells the option is accepting an ongoing obligation in exchange for a fixed amount of premium. The maximum potential gain is limited to that premium, while potential losses can be substantial. This is why short option positions generally require careful risk management, sufficient capital, and a clear understanding of the obligations involved.

Read more about Basic Option Strategies

Read more about What Influence’s an Option’s Price

Read more about More Options-based Strategies

Read more about Covered Call vs Put Selling

This material is for educational purposes only and does not constitute investment advice or a recommendation of any security, strategy, or product.

Options involve risk and are not suitable for all investors. Prior to trading options, you should carefully read the Characteristics and Risks of Standardized Options (ODD), available from your broker or at www.theocc.com.

Liquid Strategies, LLC (“Liquid”) is an independent investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”) under the Investment Advisers Act of 1940, as amended. Registration as an investment adviser does not imply a certain level of skill or training. Additional information about Liquid, including our investment strategies, fees, and objectives, is available in our Form ADV Part 2A and Form CRS.

The information provided in this material is for informational and educational purposes only and should not be construed as investment, tax, or legal advice, nor as an offer to buy or sell any security, strategy, or product. The content is provided on an “as is” basis without warranties of any kind. Although the information has been obtained from sources believed to be reliable, Liquid does not guarantee its accuracy or completeness and it may be superseded by subsequent market events or other circumstances. Liquid undertakes no obligation to update or revise any information contained herein.

Options involve risk and are not suitable for all investors. Options can be highly volatile, may lower total returns, and even well-structured strategies may result in losses due to market conditions or unforeseen events. Short options strategies involve substantial risk and may expose investors to significant or unlimited losses. Before trading options, investors should carefully review and understand the disclosure document Characteristics and Risks of Standardized Options (ODD), available at www.theocc.com or from your broker.

Educational discussions of strategies—including covered calls, put selling, spreads, protective options, volatility strategies, or execution methods—are intended to illustrate general concepts only. These descriptions are not recommendations, and actual performance will vary depending on market conditions, liquidity, transaction costs, and individual circumstances. Analytical measures and sensitivities such as delta, gamma, theta, and vega estimate sensitivity to inputs but do not predict future results.

Analogies are simplified illustrations intended to help explain options concepts. They may not reflect all risks, characteristics, or market behaviors associated with actual trading or investment strategies.

Investing involves risk, including the potential loss of principal. Past performance is not indicative of, and does not guarantee, future results. No representation is made that any strategy will achieve profits or prevent losses. Investors should consult with qualified financial, legal, and tax professionals before implementing any investment strategy.

© Liquid Strategies, LLC. All rights reserved. Not for further distribution without prior written consent.

You May Also Like

These Related Stories

Common Options-based Strategies

.png)

What Influences an Option’s Price